Wolf Richter wolfstreet.com, www.amazon.com/author/wolfrichter

Wall Street hocus-pocus has done an awesome job.

The Dow-20,000 hats have come out of the drawer after an agonizingly long wait that had commenced in early December with the Dow Jones Industrial Average tantalizingly close to the sacred number before the selling started all over again.

What a ride it has been. From the beginning of 2011 through January 27, 2017, so a little more than six years, the DJIA has soared 73%, from 11,577 to 20,094. Glorious!!

But when it comes to revenues of the 30 Dow component companies – a reality that is harder to doctor than ex-bad-items adjusted earnings-per-share hyped by Wall Street – the picture turns morose.

The 30 Dow component companies represent the leaders of their industries. They’re among the largest, most valuable, most iconic American companies. And they’re periodically booted out to accommodate a changed world. For example, in March 2015, AT&T was booted out of the Dow, and Apple was inducted into it, as its ubiquitous iPhone had become the modern face of telecommunications. New blood with booming revenues replaces the stodgy old companies. In aggregate, revenues should therefore rise, right?

And there has been a huge binge of acquisitions, from mega-deals such as Verizon’s $130-billion acquisition of Vodafone in 2013, to the many dozens of smaller companies that Apple, Cisco, IBM, and others have bought. These mergers bring the revenues of the acquired companies into the revenues of the Dow components. And in aggregate, revenues of the Dow companies would therefore soar, right?

But the other day, I was asked about the revenues of all Dow components, after having lambasted the revenue debacles of two, IBM [Big Shrink to “Hire” 25,000 in the US, as Layoffs Pile Up] and Cisco [Cisco Buys 45th Company in 5 Years, Revenues Still Stagnate].

So here we go. Fasten your seatbelt.

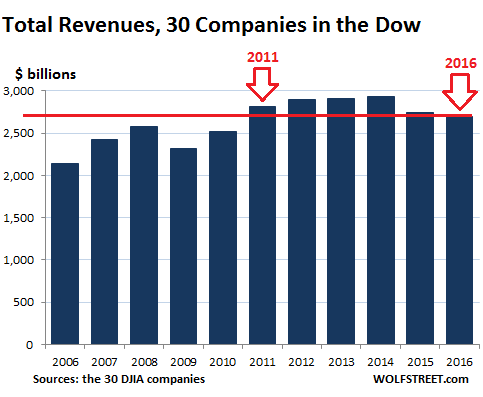

The chart below shows total aggregate revenues as reported under GAAP by the 30 companies that are today in the DJIA. This includes Apple, for example, though it only joined in 2015; and it no longer includes AT&T. For 2016, these 30 companies reported aggregate revenues of $2.69 trillion. That’s down 4.4% from 2011 and the worst year since 2010:

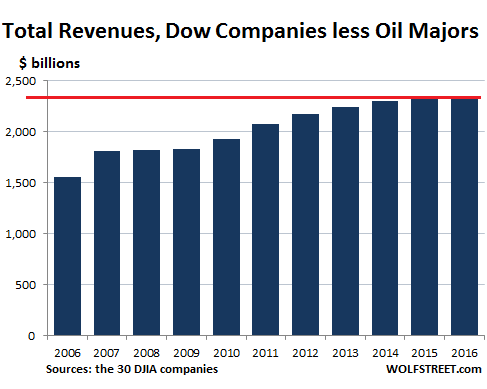

OK, you say, it’s the oil bust’s fault. The energy companies did it. Sure enough, there are two huge energy companies in the Dow, Exxon Mobil and Chevron. Alas, their revenues started dropping long before the oil bust occurred. Revenues peaked in 2011 for both of them, at a combined $740 billion. By the end of 2014, before the oil bust hit in earnest, revenues had already dropped 16% to $624 billion. And by 2016, they were down to $351 billion, having plunged 53%.

Of the Dow components, four, including Exxon Mobil, have not yet reported their earnings for fiscal Q4 2016. To approximate revenues for the fourth quarter, I took the year-over-year growth rate of the first nine months and applied it to the revenues as reported in Q4 2015. It’s not perfect, but it’s close. And given the vast aggregate numbers – trillions – any divergence for that quarter gets lost in the rounding error.

So here are the revenues of the Dow components without Exxon Mobil and Chevron:

Ah-ha, you say. It’s all the oil bust’s fault. Without the oil companies that have been ravaged by the oil bust, revenues are fine. OK, maybe not fine. Revenues without the oil bust companies are up 13% since 2011. That’s an average annual growth rate of 2.5%, barely above the rate of inflation!

But the DJIA hit 20,000 with the oil majors in the average. So in looking at the relationship between aggregate revenues and stock price movements, we need to leave them in the mix.

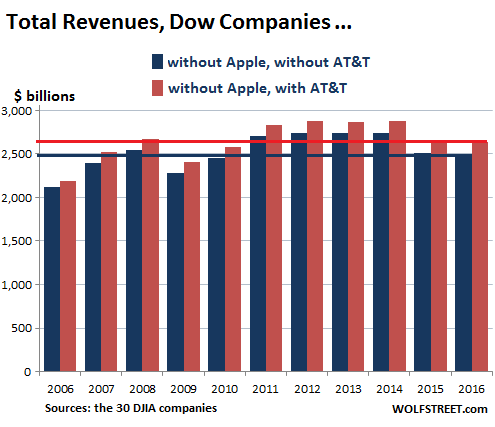

And reality looks even worse. Apple, whose revenues have skyrocketed by over 1,000% since 2006, from $19.3 billion to $216 billion, became a Dow component in 2015, replacing AT&T. And its revenues weren’t part of the 30 Dow components until 2015. So here’s what the aggregate revenues of the Dow components look like without Apple (blue columns) and without Apple but with AT&T (brown columns). A pure stagnation fest:

In both scenarios, revenues in 2016 were lower than they had been in 2008. Only 2009 and 2010 were lower. So in terms of revenues, 2016 was for the Dow components ex-Apple the worst year since 2010! And this despite the five-year binge in acquisitions!

So how have the last two years been? Don’t even ask.

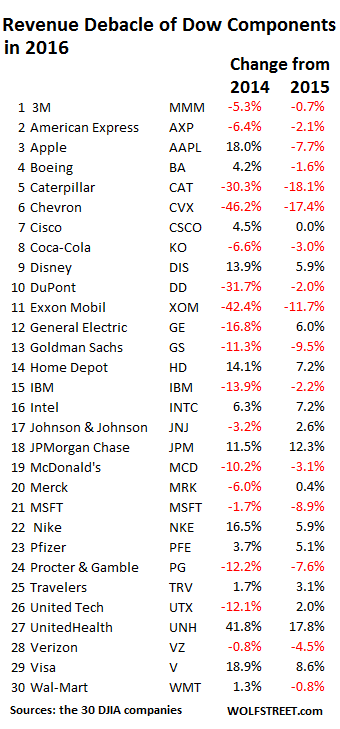

Of the 30 companies in the Dow, 16 sported declining revenues in 2016. And 17 sported declining revenues over the two-year span since 2014! Only two of them are oil companies! This table shows that inglorious list in all its beauty:

But the stock market is full of hocus-pocus, and actual revenues, as reported under GAAP, over time, are obscured the best way possible, just as magicians obscure their sleight of hand by distracting their audience with some flashy moves. So when I bring up “revenues,” everyone says, “Who cares about revenues?”

OK, I get it. It’s all about the adjusted ex-bad-items earnings-per-share – the Great American fiction – along with “leveraged share buybacks” funded with borrowed money, other forms of adroit financial engineering, and crowd-pleasing new metrics.

This relentless and eager focus on Wall Street hocus-pocus explains in part why the DJIA has soared 73% over the five years to 20,000 even as aggregate revenues, despite the delirious acquisition binge, have been mired down in a sea of stagnation.

The US economy hasn’t escaped the consequences of this corporate revenue stagnation, as hopes for a strong finish were gutted. Read… Back Below “Stall Speed”: 2016 Economy Matches Worst Year since Great Recession