“Enormous Uncerntainty.” That is how SimplyWise stated the situation in their latest “retirement confidence survey.” Such is despite a surging stock market from the March lows, trillions in liquidity support from the Fed, and a rebound in economic activity.

So, what’s the problem? Here is SimplyWise:

The current public heath, economic, and political reality in the United States has created enormous uncertainty for many Americans. A majority of citizens lack the savings to last them even three months. That savings gap is even more drastic when it comes to retirement. Indeed, the pandemic has wrought havoc on the retirement plans of many, driving some into early retirement and forcing others to postpone long-anticipated retirement plans. A majority of people today are more concerned than ever about retirement. According to the September 2020 SimplyWise Retirement Confidence Index, 58% of Americans are more concerned about retirement today compared to a year ago.” – SimplyWise September Index

Major Highlights

- Given the current economic climate, only 19% of Americans plan to invest more in the stock market. However, only 34% of households with an income of more than $100k plan to invest more in stocks.

- 40% of respondents are planning to save more.

- 51% of Americans think the stock market will decline by 20% over the next 6-months. Only 5% believe it’s improbable.

- 36% believe the economy will worsen in the next 6-months, and 28% think it will get better.

- 63% of Americans are confident in the future of Social Security if Biden is elected versus only 44% if Trump is elected.

- 86% of Americans are concerned that the current payroll tax will hurt Social Security in the long term. (90% of Dems and 83% of Republicans).

There are several critical issues in the index which encapsulate the ongoing financial distress that existing before the pandemic, but have since markedly worsened.

Financial Insecurity

Here are some additional key findings as they relate to the financial insecurity of Americans today.

- 15% of people who lost their job due to COVID-19 are now planning to retire earlier than anticipated. Just 10% in their 50s and 60s are now planning to retire earlier than expected.

- 58% of people in their 50s are not confident they’ll maintain their same quality of life in retirement.

- 30% of people in their 50s saved $0 for retirement in the last year—and 43% of them couldn’t last more than a month on their savings.

- 27% of Americans are now considering tapping their 401(k)—a pandemic high.

- 45% of Hispanics, 39% of Black, and 34% of White Americans couldn’t last a month on their savings.

- 63% of Americans feel confident in the future of Social Security if Biden is elected. Only 44% feel optimistic with the re-election of President Trump.

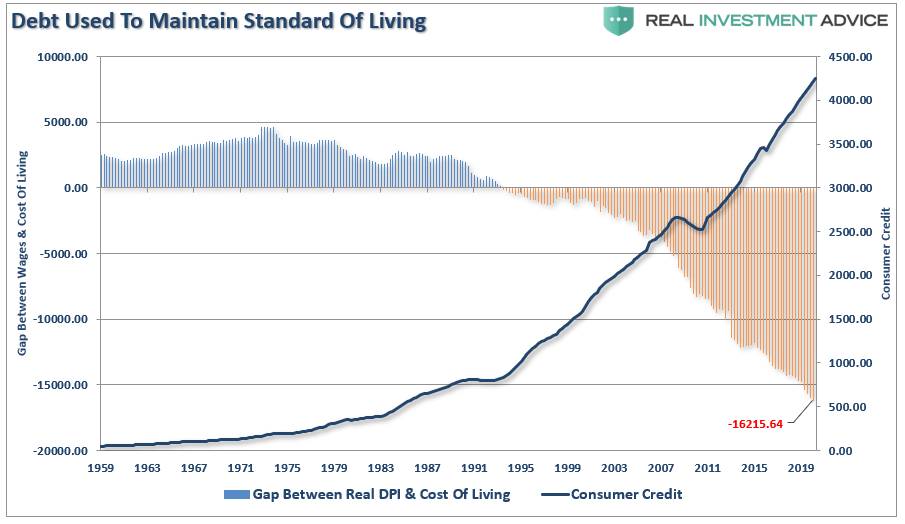

These statistics, while stunning, importantly, NOT a result of the COVID-19 pandemic. The financial insecurity of Americans is an issue that has continued to grow over the last two decades. Such is an issue we discussed in “Boomers Are Facing A Financial Crisis.”

“The lack of savings, of course, is directly related to the rising cost of living versus the lack of wage growth over the last 35-years which led to a massive surge in debt to maintain the standard of living.”

Rising Concerns Across The Spectrum

Such an inability to fill the gap between the incomes and the “cost of living,” which is evident given the surge in debt, continues to give rise to financial and lifestyle concerns. As noted:

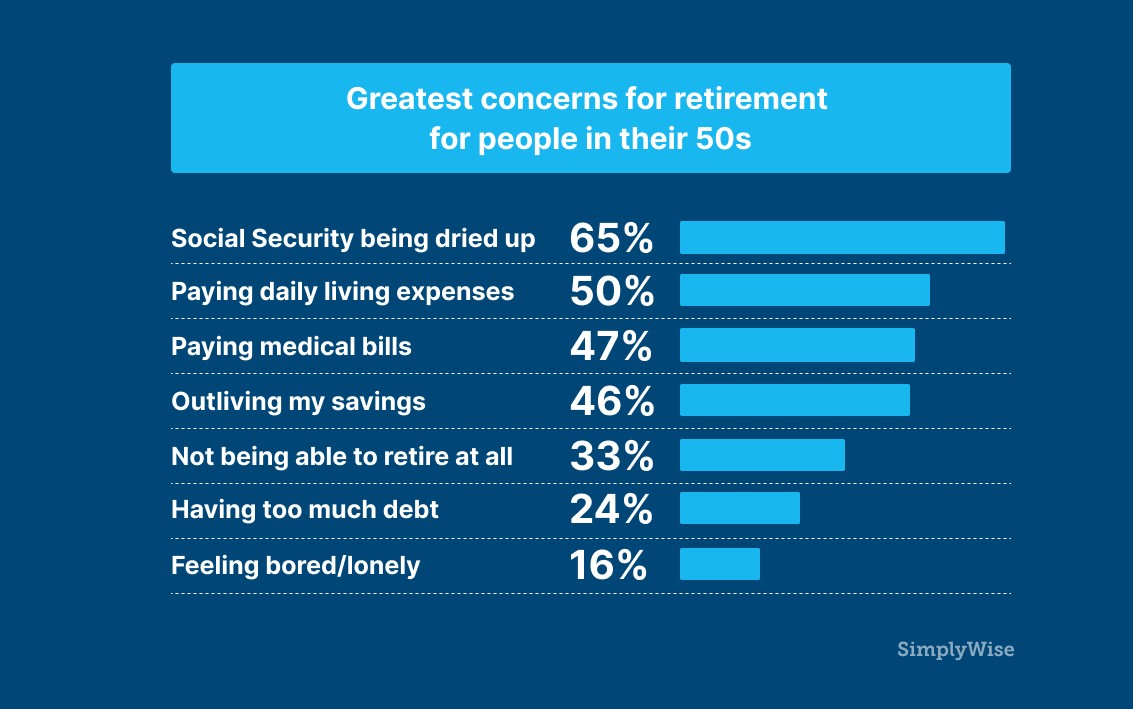

“For those not yet claiming Social Security benefits, financial concerns are among the highest anxieties around retirement. Fifty-seven percent worry about Social Security drying up, and 52% worry they will outlive their savings. For Americans who are currently on Social Security, 54% now worry about their benefits drying up—a significant increase from the 29% reported in July. Also, 47% are concerned about their ability to pay for medical bills in retirement. Another 47% are concerned about their ability to pay daily living expenses when they retire.” – SimplyWise

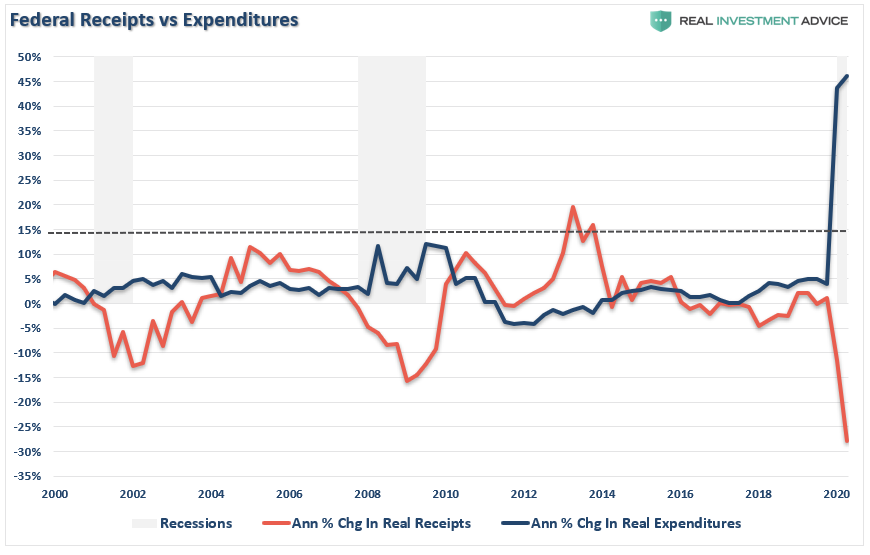

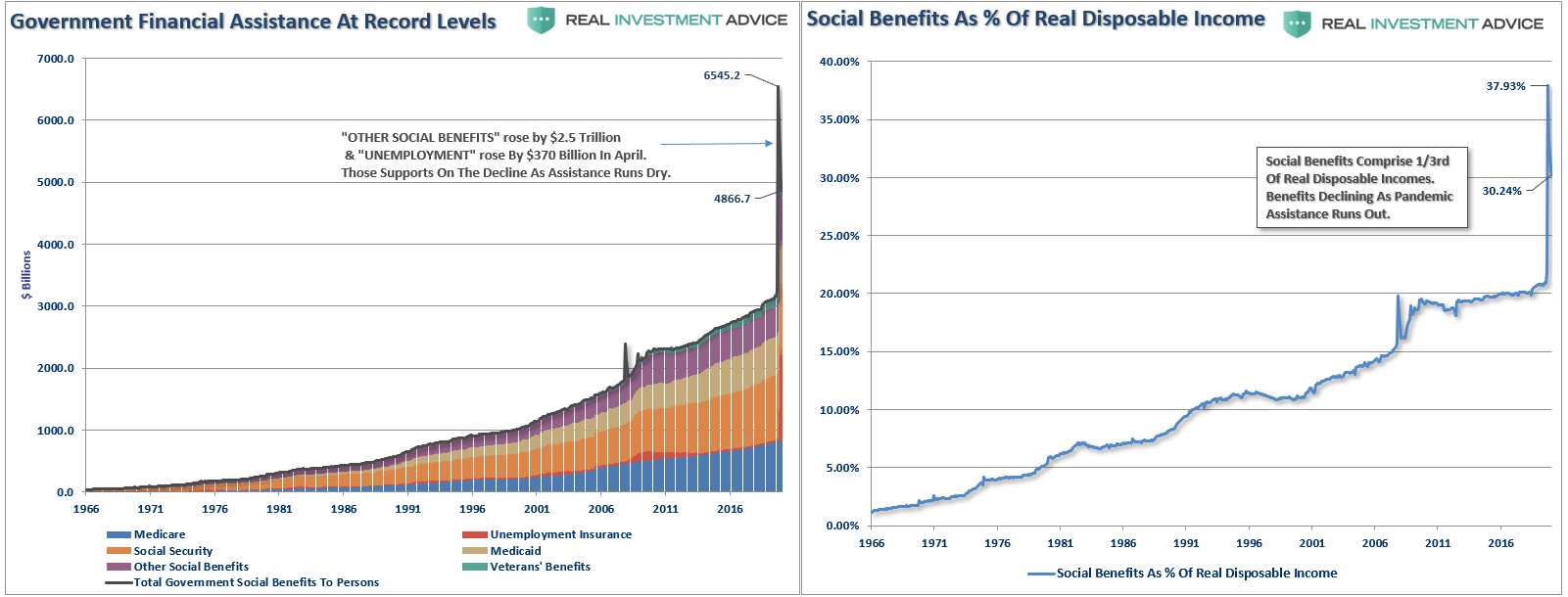

The reported problem was worst for those closest to retirement. Such is not surprising given the ongoing $70 Trillion unfunded liabilities for social welfare programs, which exacerbate each year.

The collapse in economic growth has resulted in a collapse in Federal Tax revenue needed to pay for the massive social welfare schemes in the U.S.

It now requires over 100% of Federal tax receipts to meet the mandatory spending of social welfare and interest on the debt. In other words, we are now going into debt more to provide social assistance.

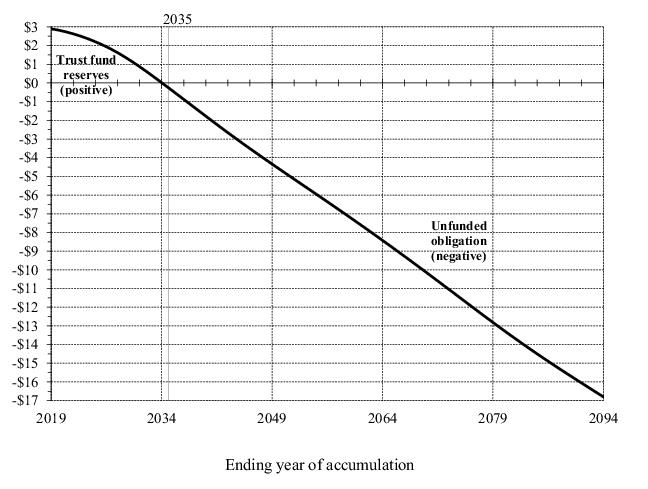

How Bad Is It?

It isn’t projected to get better.

“Steadily worsening annual balances and cumulative values toward the end of the 75-year period provide an indication of the additional change that will be needed by that time in order to maintain solvency beyond 75 years. Consideration of summary measures alone for a 75‑year period can lead to incorrect perceptions and to policy prescriptions that do not achieve sustainable solvency.” – SSI 2020 Report

“Under current law, the projected cost of Social Security increases faster than projected income through 2040 primarily because the ratio of workers paying taxes to beneficiaries receiving benefits will decline as the baby-boom generation ages and is replaced at working ages with subsequent lower birth-rate generations. While the effects of the aging baby boom and subsequent lower birth rates will have largely stabilized after 2040, annual cost will continue to grow faster than income, but to a lesser degree, reflecting continuing increases in life expectancy. Based on the Trustees’ intermediate assumptions, Social Security’s cost exceeds total income beginning in 2021, and throughout the remainder of the 75‑year projection period.” – SSA

Getting Worse

That report, dire in its warning already, was issued before the “Pandemic” and “economic shutdown.”

Meanwhile, demographics are blowing up the basic premise of the funding of Social Security. There were 2.8 workers for every Social Security recipient in 2017. That’s down from 3.3 in 2007, and that’s way down from the 5.1 workers per beneficiary in 1960.

Furthermore, the two programs function mostly as a giant conveyor belt to transfer wealth from the young and relatively poor to the old and relatively wealthy. Such allows the average person (who now lives to be 78) more than a decade of taxpayer-funded retirement.

In April, welfare spiked to the highest percentage of disposable personal incomes in history as the Government responded with massive taxpayer funds subsidies. While those numbers have declined in recent months, as the fiscal support runs dry, welfare still comprises 1/3rd of total disposable personal incomes.

“During the ‘Great Depression,’ the economically devastated masses would form ‘breadlines.’ Today, those ‘breadlines’ form at the mailbox.”

Unfortunately, recycled tax dollars used for consumptive purposes has virtually no impact on increasing economic activity. However, given the rather dire statistics, you can understand why for Americans in their 50s, 65% are now worried that Social Security will dry up by the time they retire. Moreover, 50% of them are concerned about paying for daily living expenses in retirement.

The D.A.D. Plan

The lack of financial security, and concerns over the solvency and stability of social welfare, has led to an increasing number of Americans to adopt the D.A.D. retirement plan. (Die. At. Desk.)

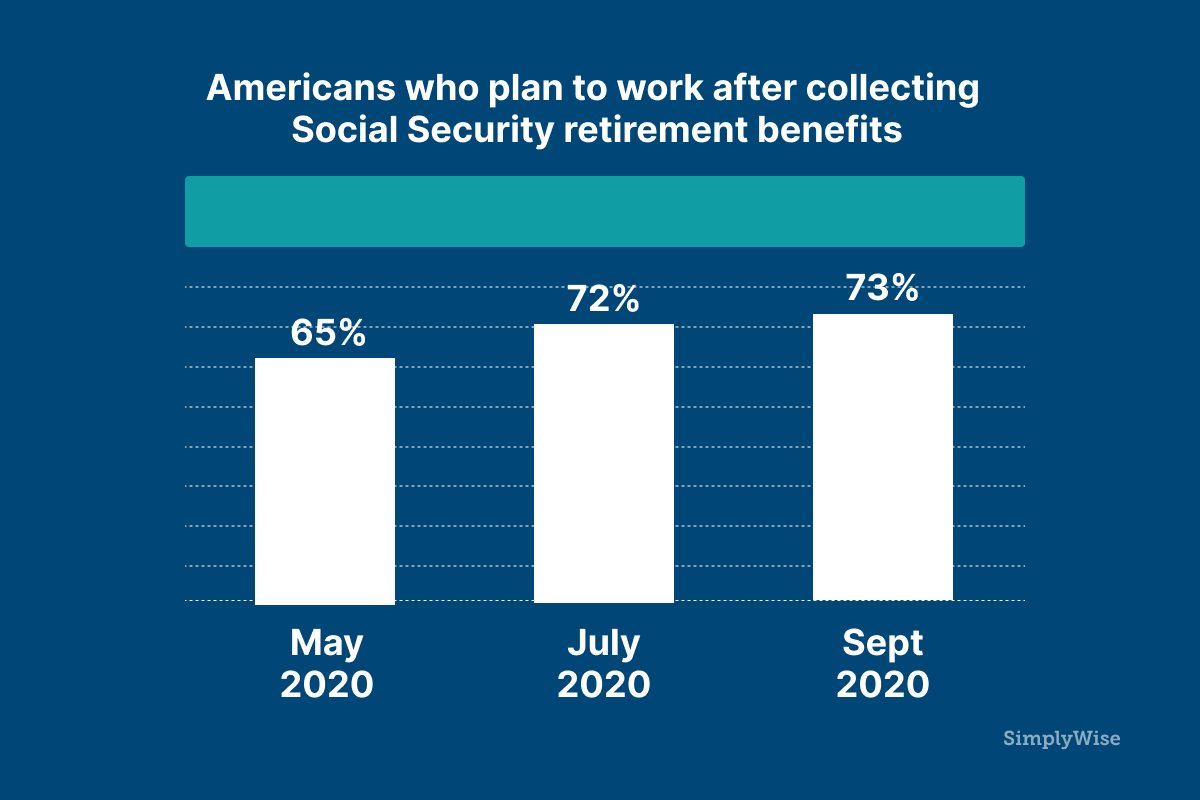

“The September Index found that more Americans than ever are planning to work into retirement. Today, 73% of workers plan to work after they claim Social Security retirement benefits. That is up from 67% this May and 72% in July. Delaying retirement may be attributed to the fact that only 63% of workers surveyed are making what they made prior to COVID-19.” – SimplyWise

We have discussed the lack of financial savings many times previously. Not surprisingly, SimplyWise noted the same in their survey.

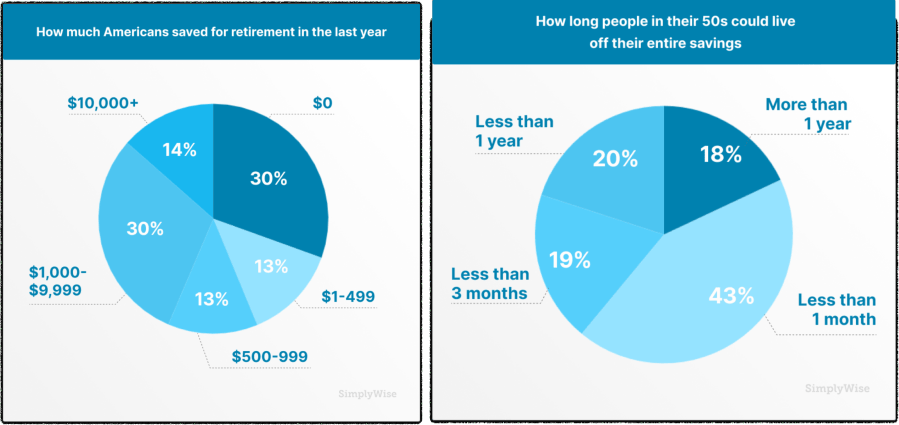

“The September Index found that 30% of Americans saved nothing for retirement in the last year. In fact, the majority (56%) saved under $1,000 in the last year. The results were similar to those of May and July, when one in three Americans saved $0 for retirement.”

The statistics are even worse for older Americans.

“Of Americans in their 50s, 30% saved $0 for retirement in the last year. And 43% of people in their 50s couldn’t last more than a month off their savings.“

These statistics are not new. However, there are far-reaching consequences on both the fiscal solvency of social welfare and long-run economic growth.

The Savings Dilemma

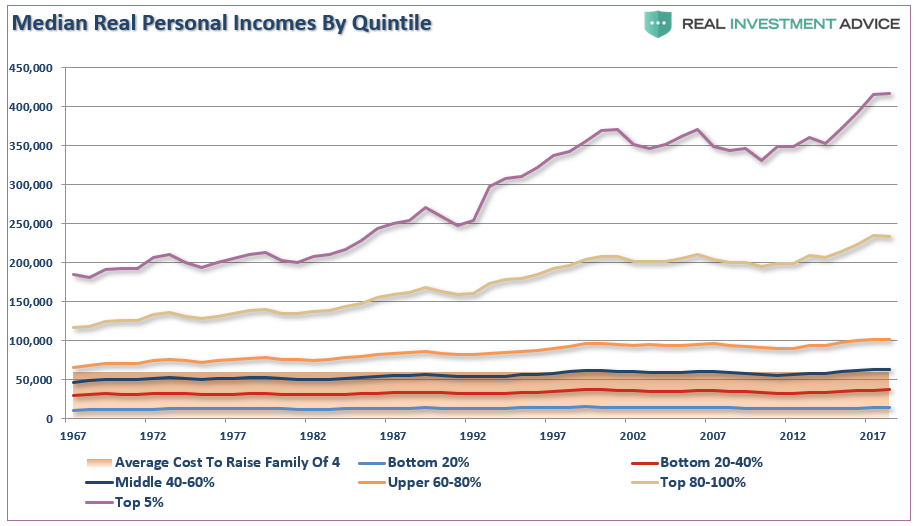

These are pretty depressing statistics when you think about it. However, for the bottom-80% of income earners whose income growth has been stagnant over the last two decades, the roadblocks to being “financially secure” for retirement shouldn’t be surprising.

In a survey from Kiplinger and Personal Capital, Americans said the biggest roadblocks to saving for retirement were:

- The high cost of health insurance. “From 1999 to 2017, the cost of family health insurance coverage has more than doubled the amount of take-home pay it consumes.”

- Disappointing investment performance. “Just under 30% of all respondents (29.4%) said that disappointing investment performance had stopped them from saving as much as they would have liked to for retirement.”

- The amount of consumer debt they carried. “21.3% of Americans said that debt, not including student loans, kept them from saving for retirement combined with the increased costs of living.”

A Market For The Wealthy

The financial “insecurity” of most Americans has been the result of decades of financial mismanagement. Stagnant wage growth, combined with a consistent relaxation of lending standards, led to three generations of Americans living beyond their means.

The problem with “living for today,’ is that it leaves you with a financially depleted tomorrow. However, the financial media is full of “pundits” and “gurus,” suggesting that if you aggressively invest in the financial markets, all your problems will disappear.

However, the problem with the thesis is it hasn’t worked out that way. Repeated crashes in the stock market have destroyed both investor wealth and confidence. As SimplyWise noted, only a small fraction of respondents were planning to invest more in the financial markets due to changes in income levels.

No Trickle Down

While the Fed keeps inflating stock markets, the “trickle-down” effect has yet to occur. Even as noted in the SimplyWise survey, “disappointing investment returns” have stunted retirees saving plans.

However, after 4-decades of transferring wealth from the middle-class to the rich, it is the top-10% of income earners who own 88% of stock markets. Therefore, it should not be surprising that most individuals planning to invest more are in the top income brackets.

For the rest, two major bear markets, lack of wage growth, and surging costs of living have eroded any ability to build savings for retirement. Such is why most retirees will depend on social welfare for 50%, or more, of their retirement income.

The mirage of consumer wealth has not been a function of a broad-based increase in Americans’ net worth. Instead, it has been a division in the country between the Top 20% who have the wealth and the Bottom 80% dependent on increasing debt levels to sustain their current standard of living.

With the vast amount of individuals already vastly under-saved and dependent on social welfare, the current economic devastation will reveal the full extent of the “retirement crisis.”

Of course, this is also why the calls for more socialistic policies continue to rise.