Cash is less of a threat to central bank policies when interest rates rise above zero.

By Don Quijones, Spain, UK, & Mexico, editor at WOLF STREET.

Sweden’s Riksbank has become the first central bank in the 21st century to take concrete measures to ensure that cash does not disappear as a means of payment from the financial system. To that end, the Riksbank proposes, in a document published on its website, to make it mandatory for all banks and financial institutions to offer cash services.

The pronouncement comes in response to a recent policy suggestion by the Riksbank Committee that only the country’s six major banks should be obligated to continue offering cash services.

That prompted a backlash from Sweden’s competition watchdog, which argued that the plan would distort competition as it would affect only a few of the nation’s banks. In response, the Riksbank has opted to apply the rule to “all banks and other credit institutions that offer payment accounts.”

There was also a difference of opinion between the Riksbank Committee and the central bank’s senior management on the issue of deposit facilities. While the Committee recommended that banks should only be obligated to provide deposit facilities to businesses, the Riksbank believes it is important for banks to also offer deposit services to individual citizens:

“This is a service that consumers can reasonably expect of credit institutions. There must also be symmetry between withdrawal and deposit facilities. In the Riksbank’s view, there is otherwise a risk that the possibilities for individuals to make deposits will decrease even further in the future. For most consumers, it would also be difficult to understand why they can withdraw cash from an account but not make deposits.”

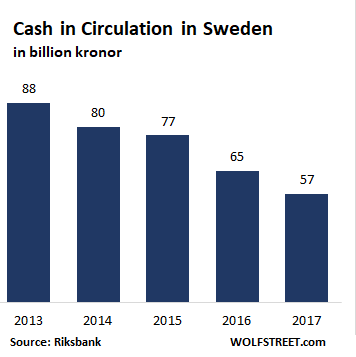

For years, the government and the Riksbank have been pushing for a “cashless society.” The Riksbank has over 1,000 articles posted on its website on the “cashless society“. The emphasis worked: between 2013 and 2017, the amount of cash in circulation dropped by 35%, earning Sweden a reputation as the world’s “most cashless nation”:

Many of Sweden’s bank branches had stopped handling cash altogether. Now, they will have to begin doing so all over again. Many of them are not happy about it. Nor indeed are Sweden’s competition and financial watchdogs, which both oppose the proposal, arguing that access to cash should be the sole responsibility of the state and not private banks.

“To secure access to cash is a collective good that the state should reasonably be responsible for,” the Swedish Financial Supervisory Authority said. It’s an opinion that’s shared by ATM provider Bankomat, which argued that it should be the state’s responsibility to ensure that citizens have access to cash since the handing of notes and coins is such an important — and expensive — part of a country’s infrastructure. Bankomat is jointly owned by the five largest banks in Sweden.

It’s not just banks that are complaining. Shops and restaurants, many of which now only accept plastic or mobile payments, could also be affected by a Riksbank proposal that retail operations deemed important to the public good, such as pharmacies, special transport services, food shops and petrol stations, should also “be included in an obligation to accept cash.”

One likely result of this is that many people who struggle to navigate the digital system, or who don’t have credit cards, in particular the elderly, no longer have to fear finding themselves locked out of the country’s payment system. Sweden’s parliament has also launched a review on the impact of going cashless too quickly as it dramatically excludes the financial needs of the elderly, children and tourists who rely on cash.

It is a dramatic u-turn for a country that not so long ago was further along the path toward eliminating cash than just about any other advanced economy. Sweden was the first European country to enlist its citizens as largely willing guinea pigs in a brave new economic experiment — negative interest rates. But a negative interest rate policy (NIRP) has its limits with consumers as long as cash remains an alternative; hence the efforts to eliminate cash.

But since then, doubts have begun to set in. In a survey earlier this year, 68% of respondents stated that they would not like to live in a fully cashless society. The survey, commissioned by Bankomat, polled over 2,000 people aged 18-65.

Incredibly, the country’s central bank, once at the forefront of the global cashless revolution, appears to agree with them. The Riksbank is now even talking about raising rates either this December or in February 2019, after keeping the benchmark repo rate at minus 0.5% since February 2016.

As the age of NIRP “gradually” comes to a close, much of the excitement about ushering in a cashless nirvana appears to be fading with it. Following on the heels of comments by senior ECB board members in defense of cashas well as an open admission by the European Commission that physical cash is perhaps not quite the source of all evil, the Riksbank’s decision to safeguard the role of cash in the financial economy is the biggest sign yet that Europe is giving up on its war on cash, and is instead allowing people switch to cashless payments systems at their own pace, however long that may take. By Don Quijones.