Do You Really Want To Be Out?

That was a comment made several times last week with respect to the markets stellar first quarter performance.

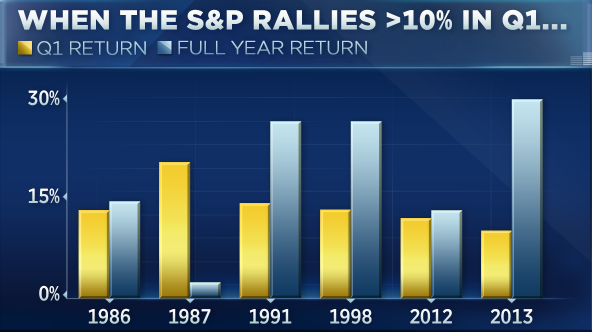

“The S&P 500 is on track for its best quarter in a decade, up roughly 12 percent. And if history is any indication, the index could be set for more gains for the rest of the year.

In nine of the 10 previous times since 1950 that the S&P returned more than 10 percent in the first quarter, it went on to post double-digit gains for the year, according to LPL Financial’s Ryan Detrick. The one exception was 1987, when the market crashed on Black Monday.” – CNBC

As we noted in this past weekend’s newsletter:

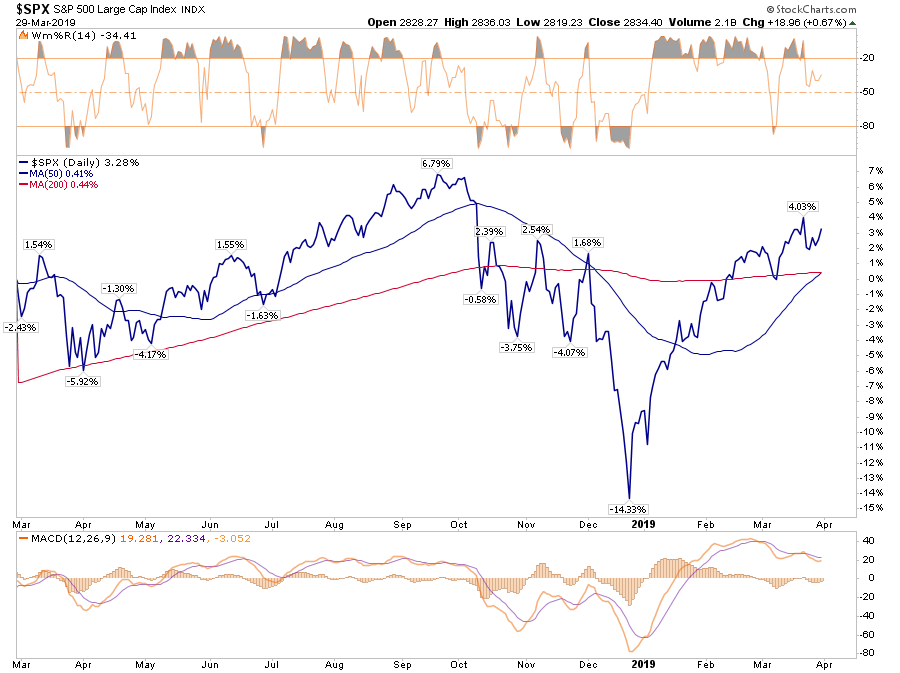

“Friday wrapped up the first quarter of 2019, and it was the best quarterly performance since 2009. As shown in the chart below, if you bought the bottom, you are ‘killing it.’”

“Most likely, you didn’t.”

Despite all of the media ‘hoopla’ about the rally, the reality is that for most, they are simply getting back to even over the last year.”

“That is, assuming you didn’t ‘sell the bottom’ in December, which by looking at allocation changes, certainly appears to be the case for many.”

So, back to our question, why would you want to be out of the market?

Here is the problem with the Detrick’s analysis above:

- 1986 – Reagan passes massive tax reform which boost stocks into 1987.

- 1987 – The market crashes.

- 1991 – The market rallies sharply coming out of recession.

- 1998 – After Long-Term Capital Management is bailed out, and the “Asian Contagion” is resolved stocks rally as the “Dot.com” bubble inflates (2-year later, investors were wishing they hadn’t bought in)

- 2012 – QE from the Fed boost stocks early in the year and Operation Twist supports asset prices through the end of the year. Balance sheet continues to expand with interest rates at ZERO.

- 2013 – In the wake of the “Fiscal Cliff” the Fed launches QE-3 to offset the risk of a government contraction in spending which turns out not to be a problem. Stocks soar on a flood of liquidity.

As I have notated on the chart below, it is important to compare the context behind historical market actions rather than just making a blanket assumption.

Case in point was the huge January rally in 2018. Headlines rang out that the January “boom” pointed to bigger gains through the rest of the year. After all, “so goes January, so goes the year.”

The year finished lower by over 4%.

So, basing investment decisions solely on previous price action without the relevant context and can lead to poor outcomes.

While it is certainly hopeful that a strong first quarter will lead to further gains for the rest of the year, the current macro backdrop is not nearly as supportive as it was previously.

- Rates are no longer zero.

- Liquidity is still being extracted through September and will stabilize, not increase.

- Economic growth is no longer-strengthening.

- Confidence has peaked

- Geopolitical tensions are rising

- Earnings growth has peaked.

- Valuations are no longer reasonable and rising, but excessively valued.

- Inflation and interest rates are no longer falling.

Well, you get the idea.

Furthermore, leading economic indicators are also signaling some concern. The chart below shows the 3-month average percentage change relative to GDP. (Try RIAPRO for 30-days FREE with code PRO30)

Yes, this current test of the “recession” warning line could turn out to be another 2012 or 2015-16 event, but as noted above, the Fed is no longer directly engaged in supplying liquidity and the Fed Funds rate is no longer zero.

Of course, assuming there is “no recession in sight” is historically what has preceded previous recessions. Coincidently, it is also the subject of a recent Bloomberg article:

“In 1966, four years before securing the Nobel Prize for economics, Paul Samuelson quipped that declines in U.S. stock prices had correctly predicted nine of the last five American recessions. His profession would kill for such accuracy.” – Simon Kennedy & Peter Coy, Bloomberg

While there are many suggesting that based on current economic data there is “no recession” in sight, therein lies the risk as noted previously:

“The problem with making an assessment about the state of the economy today, based on current data points, is that these numbers are ‘best guesses’ about the economy currently. However, economic data is subject to substantive negative revisions in the future as actual data is collected and adjusted over the next 12-months and 3-years. Consider for a minute that in January 2008 Chairman Bernanke stated:

‘The Federal Reserve is not currently forecasting a recession.’

In hindsight, the NBER called an official recession that began in December of 2007.”

For investors, while the first quarter of the year was a massively strong reflex rally from the lows, the risk of expecting asset prices to continue to rise unabated may prove disappointing. This is particularly the case as the factors which drove that first quarter performance are unlikely to repeat in the months ahead.

In December there was:

- Deeply negative sentiment of the markets

- Asset prices were stretched to the downside

- The Fed surprised the markets with a very dovish reversal

- The White House surprised the markets with statements a “Trade Deal” was near.

- Oil prices had declined to lows, were oversold, and prime for a rally.

Today:

- The markets are no longer fearful as shown our RIA PRO Technical Index

- Asset prices are now stretched back to the upside

- Economic data has bounced but remains weak

- The Fed has more room to disappoint than not with future announcements. While many are expecting a rate ease later this year, such is unlikely to happen before data materially worsens.

- There has been no “trade deal” completion

- Oil prices are overbought and extended to the upside.

This was also the subject of a WSJ article by Ira Iosebashvili on Monday:

“Investors hoping for stocks’ rally to keep up the first quarter’s pace may be headed for a disappointment. Big climbs in the S&P 500 have tended to slow or even reverse in the three months following a first-quarter rally of 10% or more, according to Dow Jones Market Data.”

“Often, the gains pause as investors grow wary that prices have risen too high, or concerned that the expectations driving the rally won’t pan out. Some investors tend to lock in profits after a particularly good quarter, pushing markets lower.

Earnings are another factor that could pressure stocks. Some investors are worried that a slowing U.S. economy is already weighing on corporate bottom lines and clouding the case for share prices to keep rising. S&P 500 companies are expected to report a nearly 4% drop in first-quarter earnings from a year earlier, according to FactSet.”

“But if I did get out now, I might miss some of the upside.”

Such is really a personal choice, but as I stated earlier this year, there is a very high probability the bulk of the gains for this year have already been made.

However, the emotions of “greed” and “fear” are extremely powerful forces which consistently lead to poor outcomes over longer-term periods. As Michael Lebowitz and I discussed in our VideoCast last week, there is a time to be a contrarian and Howard Marks, the head of Oaktree Capital Management, just recently sold his entire firm. Howard is the ultimate contrarian investor and the message should not be readily dismissed.

This was the same message Sam Zell sent when he sold EQ Office to Blackstone Group in 2006 for $36 billion in the largest leveraged buyout in history at the time. Or, just as timely was when Bobby Shackouls, the CEO of Burlington Resources, sold to Conoco Phillips. Both occurred just prior to the “Financial Crisis” and the crash in oil prices.

Were they just lucky, or did they see something the rest of us didn’t?

There was “no recession in sight” at the time. The economy was growing, stock market prices were rising, and it was a “Goldilocks economy.”

But to this point was David Rosenberg’s missive yesterday which stated quite elegantly:

“I have to say, that from a contrarian perspective, when an article like ‘Investors Rush To Buy Up Stocks’appears on the very front page of the Wall Street Journal, you know a whole lot of good news is in the price. It conjures up the image of two of Bob Farrell’s famous Ten Market Rules to Remember: #5 – the public buys the most at the top and the least at the bottom, and #9 – when all the experts agree something else is going to happen.”

While hindsight is pretty clear about what happens given the current environment of weak economic and profit growth, combined with high valuations, and deteriorating technical underpinnings, the ultimate outcome could take months to develop.

And because a warning doesn’t immediately translate into a negative consequence, it is quickly dismissed. It is akin to constantly running red lights and never getting into an accident. We begin to think we are skilled at running red lights, rather than just being lucky. Eventually, the luck will run out.

So do you want to be out? Most will say “no.”

Just for the record, we aren’t “out” either.

But if you are waiting for someone to tell you the recession has officially started, it really won’t matter much anyway.