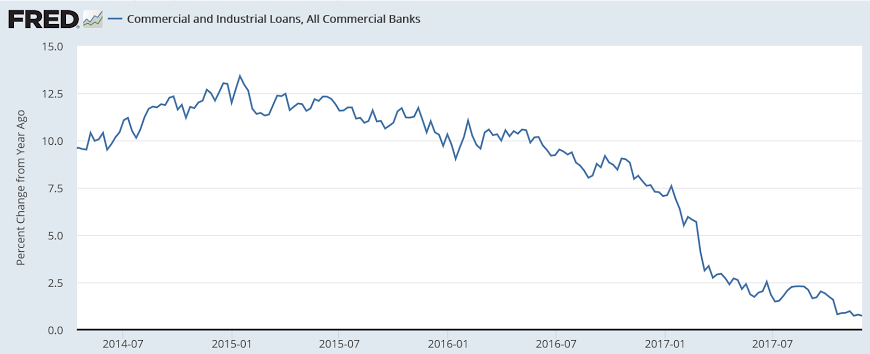

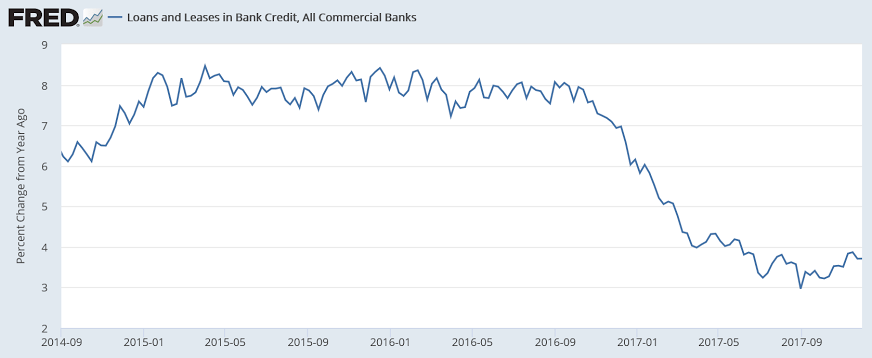

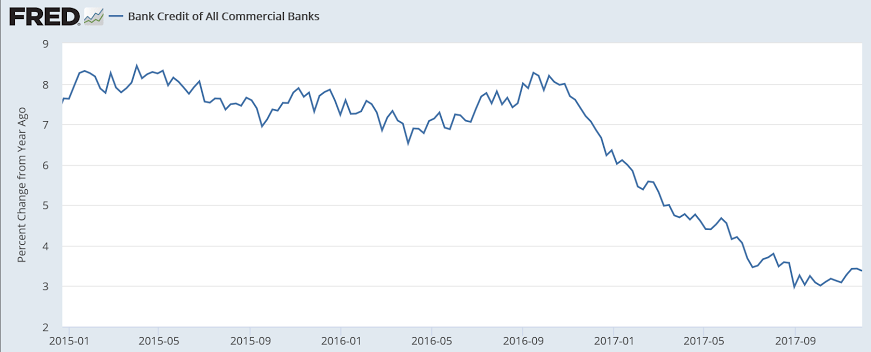

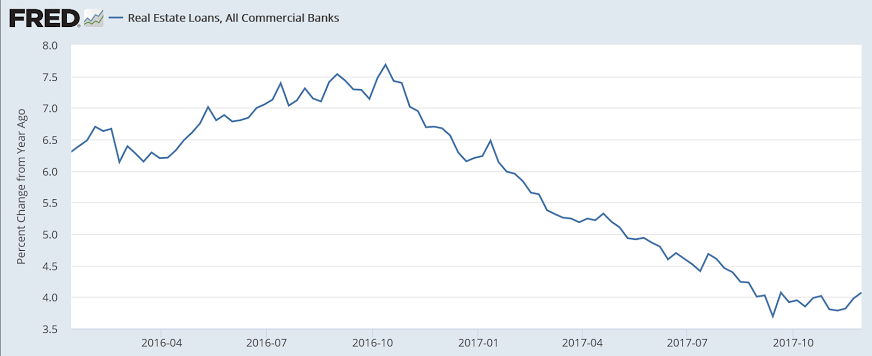

Something happened about the time of the Presidential election that caused a sudden deceleration of bank lending, which had already been decelerating since the collapse of oil capex.

And still no signs of a recovery here, as consumers seem to be instead dipping into savings to sustain consumption as personal income growth decelerates as well:

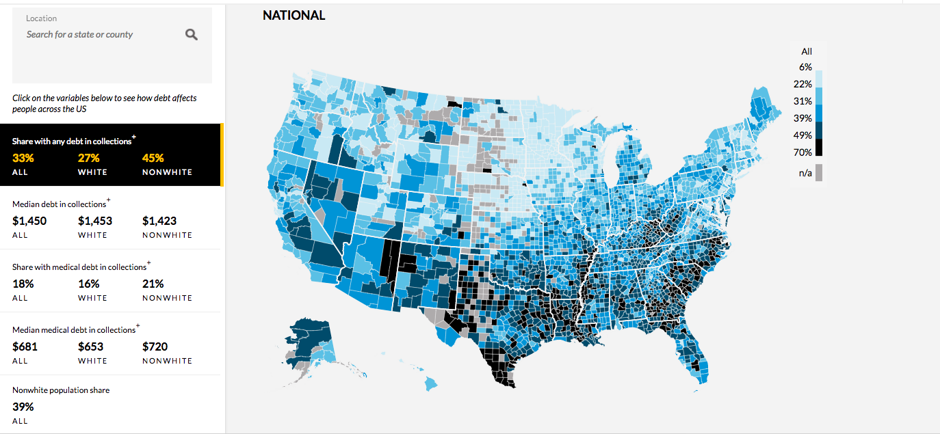

Not much unites Americans these days, except, perhaps, past-due bills. A third of American households are currently in debt, and in the second quarter of 2017, they owed a record $13 trillion altogether.In a new interactive map, researchers at the Urban Institute visualize how this massive debt burden varies by geography. The map is based on 5 million records sourced from a major credit bureau, and shows each county’s share of households that have their debt in collections. The darker the color, the higher the concentration of people who haven’t been able to pay what they owe, from credit card and medical bills, to parking tickets to child support.

After the institutions these people owe moneyto send their case to a collections agency, their financial situation can go even further downhill: their credit scores can suffer, jeopardizing, among other things, the ability to borrow money, rent or buy homes, and be eligible for certain types of jobs. In other words, having debt in collections has longterm and far-reaching effects, explains Signe-Mary Mckernan, co-director of the Center on Labor, Human Services, and Population at the Urban Institute. The upshot: Not a single county in America is debt-free, according to this UI map.The extent of the borrowing, however, is dramatically different between states. Louisiana, for example, has 10 times more households with debt in collections (30 percent) than Minnesota (3 percent). In general, the South appears to be drowning in debt, with shares higher than 50 percent in places like Deaf Smith County in Texas and Carter County in Kentucky.A screenshot of Urban Institute’s interactive map. Click through here to zero in on your county.

In the past, large gaps between consumer confidence and the savings rate were followed by sharp declines in consumer spending. Will the US repeat this pattern? t.co/pfk74qyhGI via @SoberLookpic.twitter.com/KB6UzyS15b

Few make money-related New Year’s resolutions — despite record debt and low savings. Here are 5 apps to help you stick with resolutions.

New year, same old finances.

Only about one in four Americans (27%) say they will make a financial resolution this year — an all-time low and down from the 43% who vowed to do so in 2014, according to data released Monday from financial company Fidelity.

“While the market has reached all-time highs this year, financial new year’s resolutions have slipped to an all-time low,” said Ken Hevert, senior vice president of retirement at Fidelity. “Part of the reason these resolutions are on the decline is because so many people are feeling better about their personal financial situation and are optimistic about what 2018 will bring.”

This comes at a time when more of us than ever may need financial resolutions: Credit card debt hit a record high in 2017, with more than $1 trillion being owed, according to the Federal Reserve. Student loan debt has jumped 150% over the span of just a decade. And we’re not saving much either. About 1 in 4 Americans don’t have a single dollar saved for an emergency.