by David Haggith

Bloomberg this week ran a story telling us how the smart money gets out of the stock market when it hits its all-time peak and how the dumb money helps the smart money out. Only they didn’t know that was what they were writing. It typically happens this way:

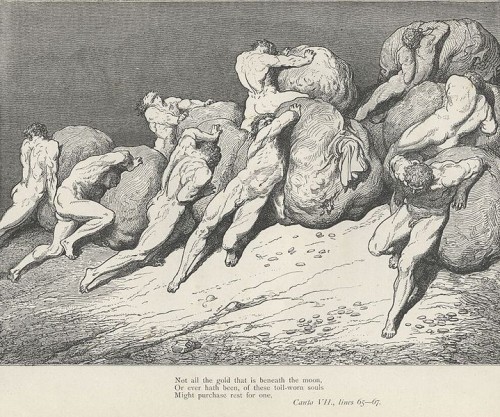

At the end of a deliriously euphoric market rally when the market is preparing to crash, all the Joe Sixpacks, mom and pop and the family dog open trading accounts and try to chase the tail of market action. Many throw in their entire retirement funds, pawn the dog’s collar and take out loans on credit cards to buy in as much as they can. By buying in late, they help provide a smooth exit for the smart money. At least for some of it. It is the little guys, tough from hard labor, whose muscles are employed to push the money bags of the rich to the top of the mountain from which the little guys are allowed to jump off.

That appears to be happening right now. While retail investment (at the mom-and-pop level) in stocks mushroomed last quarter, household debt also mushroomed, jumping at an annual rate of 5.2%, which is the fastest pace since …. 2007. (There is that comparison we keep finding in data everywhere.) Consumer credit rose at an annualized rate of 7.8%. Consumer credit-card debt just topped out at over a trillion dollars, and savings at the same time bottomed out to one of the lowest rates in history.

It’s hard to say with certainty what all that debt all those savings were used for, but the change in both certainly matches the pace of growth in retail stock investments. (The S&P 500 rose 6.1% last quarter, with much of the new money pouring in from retail investors.) With no hard connection in those numbers at my immediate disposal, it would be a fallacy to claim them as proof that people are taking out credit card debt and depleting their savings to buy stocks, but that correlation certainly matches up with anecdotal accounts that many stock brokers are reporting at the street level.

All Trumped up and nowhere to go

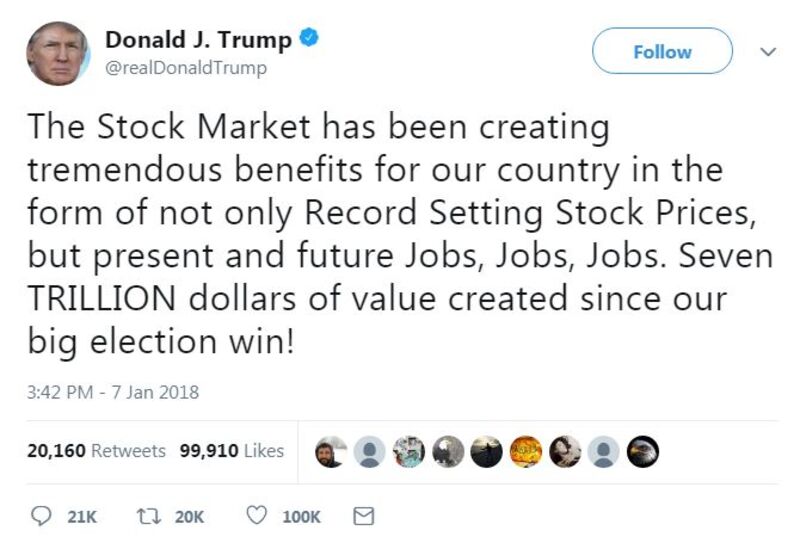

Certainly the roar of mom and pop into retail stock investing is happening now …. big time, big league, in a hyuuuge way with the Donald’s supporters being the ones who are rushing headlong in to provide the gold-bricked exit path for the 1%:

As 2017’s roaring bull market gives way to a markedly choppier 2018, the buzz among Wall Street stock touts is that the best of the Trump Trade has passed…. Don’t try to tell that to the true believers in San Angelo, Texas. Or Covington, Louisiana. Or Sioux Falls, South Dakota. They’re sure this rally has just begun, and they’re sure they know why. “I hear it every day,” said Jimmy Freeman, a financial adviser at Edward Jones … east of the booming Permian Basin shale oil fields. “The market’s going up because of Trump….”

Across middle America, in the towns big and small that voted overwhelmingly for Donald Trump, his most ardent, and financially comfortable, backers are opening stock-market accounts or beefing up existing ones, according to interviews with more than a dozen advisers and brokers. They were spurred on by a stream of presidential tweets crowing about, and taking credit for, the gains throughout 2017 and they remain undaunted now as the rally sputters and the tweeting dissipates. (Bloomberg)

Yes, the Trumpettes — by which I mean the little guys who supported the Donald because they were stomped all over by Bush and Obama — are now flooding into the market to provide the essential other side of the trade needed in every market sell-off — buyers. It’s a market maxim that you cannot have a market sell-off without a lot of buyers willing to leap for falling prices.

…From what financial advisers in conservative areas are seeing, there is a Trump-minted rush. Clients … at Concho Investment Advisors in San Angelo “are now more inclined to invest into riskier assets like the stock market” … and many cite the president. Todd Neff, for one, has put $400,000 into stocks since Trump’s election. Before, he wasn’t much of an investor, basically topping out his out his 401(k) and dabbling in shares here and there. A sheep breeder and small-business owner in San Angelo, he said he would have “dropped back big time” if Hillary Clinton had won. Consumers’ confidence in the stock market soared to a record high in January before fading in February…. Among Trump’s fans, though, trust in the firebrand politician as a stock-market bulwark easily endured the selloff

Share buybacks surging

That’s one side of how the smart money gets out at the last minute and winds up richer than ever: they are helped by the good-meaning people who hope to get a last piece of the action — this time from the champion they elected and believe in. The other side is orchestrated by the executive rats who flee their own sinking, stinking corporate stocks by using the company money to buy back their own shares. That’s the bigger action. And that appears to be happening on steroids right now, too.

As the stock market roars toward its triumphant collapse, you hear the big-name analysts talking about how stocks are not overvalued because “earnings are doing great. They’ve never been better.” What they usually mean is earnings per share, and what is really doing better in that fraction is the denominator. The number of shares is shrinking as corporate boards make decisions to drain the company coffers in order to buy back shares … often from themselves … sometimes even in special deals offered only to themselves off the general market (as I’ve reported in the past).

Buybacks have a double edge of cutting power. First, they cut the number of shares over which earnings are divided, making “earnings” look stronger; but secondly, they create their own market demand. Increasing demand = increasing price:

Over the past decade, there has been no corporate instrument of mistruth more powerful than buybacks, an issue we have dissected in these pages for years. U.S. firms have spent roughly $4 trillion on buybacks since 2009, making corporations the biggest single source of demand for U.S. shares…. Buybacks have “accounted for +40% of the total earnings-per-share growth since 2009, and an astounding +72% of the earnings growth since 2012. (13D Research)

What better plan could there be for the smart money, which owns the major shares, to exit the market without crashing the value of their own shares than by creating demand from within the company the smart money governs to buy shares in numbers equal or greater to all those the major investors wish to sell? (Major investors being the ones who sit on the board or hold executive positions.)

Thanks to Trump’s new tax law encouraging repatriation of cash that has been stored overseas, companies are doing exactly what I and many others said they would do with their one-time tax savings on this mother load. No, they are not using it to invest in their own companies as proponents of the plan promised, and as I predicted they would NOT do. They are using their overseas cash stockpiles buy back stocks.

Buybacks are already on record pace?—?$171 billion worth have been announced so far in 2018, more than double the amount disclosed by mid-February 2017. If a tax-bill-fueled buyback bonanza can effectively “buy the dips”, market tranquility can be protected, preventing a large-scale unwinding.

In fact, the first six weeks of announced buybacks this year already was higher than the entirety of 2009. JP Morgan projects that, at this rate, S&P 500 companies will by back a record $800 billion in stocks in 2018. JP noted that large accelerations in buybacks like this tend to happen during market selloffs and for that reason says that buybacks could go higher than $800 billion this year if they rise to the level seen right at the end of the last business cycle where companies returned more than 100% of profits to shareholders.

These enormous buybacks are the only action saving the market right now from crashing. The Trump cash cache came through just in time to offset the initial stages of the Fed’s quantitative tightening. Of course, that was also my basis for predicting that the market would likely plunge in January but that this wouldn’t be the big collapse … not yet.

That collapse, I maintained, will come in the summer when much of the cash repatriation is winding down, just as the Fed is stepping its own unwind up to third gear. At about that point this year, the Fed’s reduction of its balance sheet and the effect of rising interest rates could outstrip the pace of buybacks and other benefits the market gets from the new tax plan. So, that’s the basis for my giving that timing.

Analysts estimate $200 billion in buybacks from cash repatriation and $100 billion in buybacks funded by tax savings. I see the $450 billion in Fed bond sell-offs as playing against that flood of investments by raising interest on bonds. If JP Morgan’s prediction of $800 billion in buybacks is right, then I’ll be wrong about the Fed taking the wind out of the stock market and the general economy that soon; but I think rising interest will turn back the flood tide of buybacks later in the year by stripping away their easy funding, so that they wind up not happening in the big numbers that are being projected. (There is a dynamic involved that I think those who are promising the buybacks are not seeing.)

David Stockman sees it and projects the current buyback rate would hit even higher than JP does — at a record $1 trillion this year — except that, like me, Stockman doesn’t see the current rate as being sustainable.

To be sure, we don’t believe they will ever get there because the bond “yield shock” is going to be sobering up corporate boards right soon. (TalkMarkets)

I agree. As you can deduct from the following graph, much of the buyback action during the so-called “recovery” period was financed from debt (largely corporate bonds) prior to the Trump’s tax changes:

Buybacks happen the most right at the market’s peak as the market tries to sell off to try to delay the sell off (so the smart money can get out), but then fall off quickly with the market once all hope is gone.

The drainage of the bulk of Trump’s tax benefits that is now running straight into the buyback pit (as I predicted it would) is already causing a backlash among politicians as they learn what nonsense the talk was of using that money to develop businesses, build new plants, develop new products and … the biggest lie of all, boost wages. Some of us pay attention to history — learn from it — so knew from the beginning that those promised were completely bogus.

Since passage, total buybacks announced exceed worker bonuses and raises by roughly 63x.

Yes, the dollars spent on buybacks amount to only 6,300% more than the bonuses and wage boosts that have been announced. And who benefits from all of that?

The smart money.

The CEOs and other top managers who receive much of their compensation over the years in stock options and the board members and other shareholders in the company. But, hey, if you got your thousand-dollar bonus, what is to complain about, right? That ain’t crumbs.

Well, not to you maybe, but it is mere dust under the table compared to what the shareholders are getting. God rest their merry souls … hopefully for a very long time.

The nice thing (for them) is they are also able to use that repatriated money and their corporate tax savings to bail themselves out of all that debt they used in preceding years when interest was cheap to drive their stock prices up:

According to an IMF estimate from last spring: “Large U.S. corporations have experienced a negative net equity issuance of $3 trillion since 2009 due to share buybacks.” U.S. corporate debt?—?piled on by both strong and weak hands?—?sits at an all-time high of $13.7 trillion.

If they want to. Or they can just jump ship and leave the corporation buried in debt. What do they care if they sell their shares first?

Meanwhile, the tax bill will disproportionately benefit the strong hands?—?for one, the richest 10% of companies control 80% of the $1 trillion offshore cash hoard.

Uh huh.

Since 2009, the largest equity drawdowns?—?August 2015, January to February 2016, and two weeks ago?—?all occurred in or right after the share buyback blackout period. Even less surprising, corporations stepped in after February 5, 2018, bought the dip, and suppressed volatility. Goldman Sachs’ unit that executes share buybacks for clients had its busiest week ever, seeing roughly 4.5x its average daily volume over 2017.

Uh huh.

That’s where I said the vast majority of the repatriated money would go.

Share buybacks are a major contributor to the low volatility regime because a large price insensitive buyer is always ready to purchase the market on weakness.

Those companies that don’t have the free cash that the top 10% of companies have will not be able to keep inflating their stock values against downward market forces, and will be the first to start sliding away, taking more and more of the market with them over time.

Said Moody’s in the article referenced above,

High quality companies will benefit but low-quality levered companies could get hit hard.

The highly levered companies that used debt to do buybacks during the “recovery,” are most likely not the companies with cash stockpiles overseas that can now be repatriated cheaply. Now, that interest rates are rising, they will get caught in a debt trap and hammered badly.

So, here we go over the Niagara falls of debt … again

Because assets are bundled, it may take dangerously long to identify a toxic asset. And once toxicity is identified, the average investor may not be able to differentiate between healthy and infected ETFs. (A similar problem exacerbated market volatility during the subprime mortgage crisis a decade ago.) As Noah Smith writes, this could create a liquidity crisis: “Liquidity in the ETF market might suddenly dry up, as everyone tries to figure out which ETFs have lots of junk and which ones don’t.”

Been there, done that, learned nothing.

Did you know that buybacks used to be illegal in the United States because regulators feared corporate boards would use them to manipulate the prices of their own shares?

Go figure, huh? What a dumb idea! Nobody would do that, so let’s deregulate it!

That buyback regulation that was removed is now an area of law Democrats are focusing in on for the mid-term election cycle. If the law reverts to ending buybacks, the low-volatility regime ends with it. But don’t worry. If the Dem’s don’t get elected in sufficient numbers to reinstate that regulation, rising interest rates will accomplish the job anyway as soon as that hoard of repatriated cash runs out. You can only dam against the tide so long before market forces have their way.

The exodus is underway

So, that’s how the smart money gets out of the stock market, leaving their ultimately devalued stocks in the hands of the dumb money.

As the Financial Times humorously noted,

Flush with cash after the Republican tax cuts, Cisco announced on Wednesday that it was building gleaming factories across the US, employing hundreds of thousands of workers to make the latest cutting-edge routers…. Sorry, of course not. The money is going back to shareholders.

Yeah. That’s the way the real world works these days. Sorry wage earners. You get the crumbs after all.