The Roaring Volatility Is A Special Nightmare For The Beloved $2 Trillion Short Vol Trades And Forced Liquidation Of Short Volatility ETNs (XIV) Could Cascade Into A Stock Market Crash

Of all the harrowing things seen in the stock market Monday, one was a special nightmare for investors in what has become one of the stock market’s favorite strategies.

It’s short volatility, a bet against equity turbulence that traders have been piling into for years, lifting assets in related exchange-traded products to more than $3 billion, a record. Estimates of how much money is tied up in the tactic overall vary but one estimate from Chris Cole of the Artemis Capital Advisers hedge fund puts the total at more than $2 trillion.

The Cboe Volatility Index’s biggest rally ever is raising thorny questions about the future of exchange-traded products tied to the gauge.

An ETP meant to mirror moves in the front of the VIX’s futures curve plunged more than 75 percent in after-hours trading following an 80 percent spike in contracts that comprise its underlying index during the trading day, potentially putting in play triggers that would enable the fund’s owners to liquidate it to avoid losses.

Nicole Sharp, a spokeswoman for the note’s sponsor, Credit Suisse AG’s VelocityShares, said in an emailed statement that “The XIV ETN activity is reflective of today’s market volatility. There is no material impact to Credit Suisse.” She didn’t elaborate on the fate of the product.

XIV is highly likely to have triggered an Acceleration Event / Liquidation Event today

Based on data provided by Velocity Shares ETNs, XIV closed on Friday at $115.55. During market trading today, the price closed at $99.00. However, immediately after the close, prices of XIV began to plummet and currently trade at $15.43. This represents of over 86% in a single day.

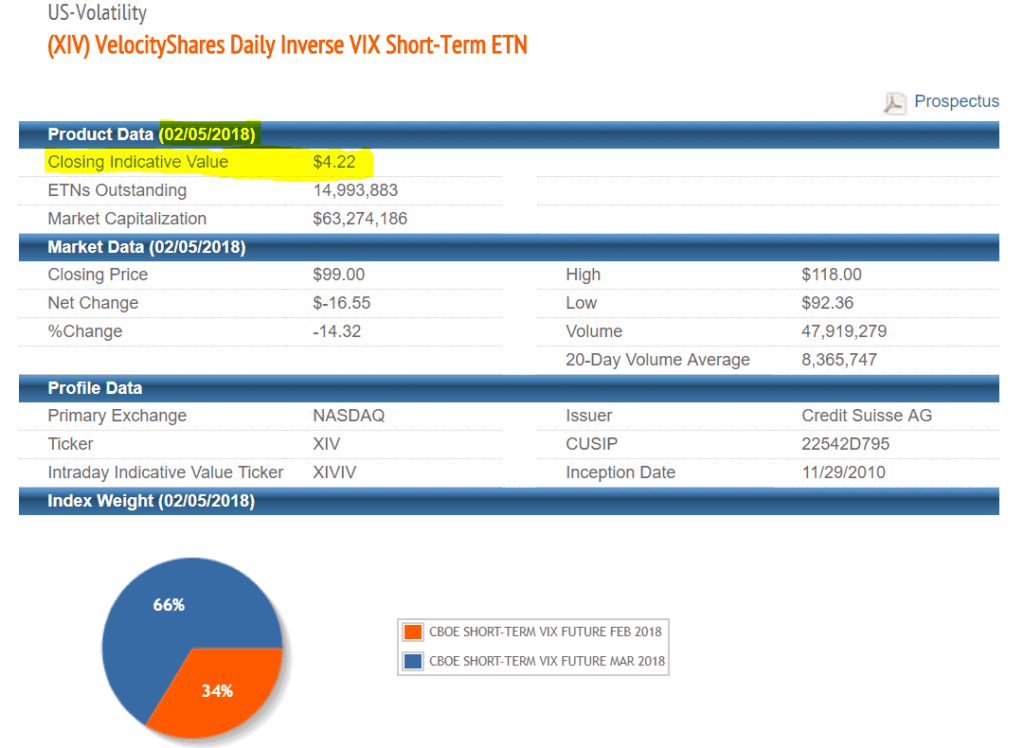

However, that doesn’t tell the full story. Market price is not the important factor. Instead, the important piece is the “Intraday Indicative Value.” As we see in the image below, XIV ended trading today, February 5th, 2018 with a closing Indicative Value of $4.22. Although I lack data on the closing indicative value from Friday, we can assume it is fairly close to $115. Based upon that, we see that the indicative value has a loss of approximately 97%. ($4.22/$115)

The Closing Indicative Value represents the -80% loss threshold for an acceleration event or liquidation event. (Source: VelocitySharesETNs.com)

Negative Fallout: Cascading wave of selling which could lead to a Stock Market Crash

The result of all of this is likely a stock market crash. Let’s walk through the process. There are two parts: retail and institutional.

The retail effect is fairly straightforward:

First, XIV shareholders are liquidated. Either at or near Net Asset Value which represents an 80-100% loss.

Second, margin calls affecting some XIV holders will force them to sell any and all assets, including stocks, to raise cash to meet their margin calls. This will promote initial selling pressure.

Third, large selling pressure across the board will make many investors cautious to buy into an ongoing crash, reducing bid liquidity.

Fourth, an initial decline triggers stop-loss trading strategies to sell at a loss removing further liquidity from the market.

Finally, the ongoing decline causes an even larger rise in volatility, and hedge funds, pension funds, and corporations with secondary exposure to short volatility become impacted. The cycle then repeats.

The Institutional Impact of Short Volatility Risk Covering

Institutional effects are a lot more complicated, but they might also have the greatest impact. Remember that all of these short volatility funds are actually trading in the volatility futures market. At first, it might seem like the futures market is completely independent of the stock market itself. However, that would be a mistaken assumption. Trading in the futures market has an indirect but critical impact on the stock market itself.

While the volatility index is unable to be traded directly, this is not true for the stock market index. The stock market index can be traded in four different ways.

Buy the stock market index itself such as the SPY ETF.

Purchase each individual stock in the stock market index.

Buy options on the stock market or individual stocks.

Trade stock market futures that settle against SPY.

Institutional investors such as Hedge Funds, Pension Funds, and Corporations can Arbitrage differences in ETFs, Options, and the underlying stocks

Remember that at the end of the day, buying through any of these four methods still results in essentially buying ownership of the underlying companies. Yet, the ability to buy those companies in different ways allows large institutional investors to arbitrage differences in the prices allocated within any of the four avenues against each of the others.

Basically, if S&P 500 trades at $2600 while the S&P 500 futures contract trades at $2700, an institutional investor can buy the S&P 500 index (SPY) while selling the S&P 500 future and pocket the difference of $100 as profit.

This relationship works great most of the time. However, in a black swan style event such as the forced liquidation of XIV, this can have devastating consequences.

XIV Liquidation is a Black Swan event for the Stock Market

Let’s discuss the institutional fallout of XIV’s liquidation.

The XIV fund along with its fellow short volatility funds like SVXY were *Short* volatility futures. I know this is a given, but it’s important. Because XIV was short the futures, they were forced to buy back a huge number of futures contracts after the stock market closed in order to cover their short position. According to Pravit_C on Twitter courtesy of Robin Wigglesworth, XIV and SVXY had to purchase approximately 200,000 VIX futures contracts.

That is the definition of a short squeeze.

Unfortunately, that means other people sold 200,000 VIX futures contracts in that time frame. Those futures contracts are the spark that lights the fire of my cascading effect proposal.

The Futures market can lead to massive selling pressure in the Stock Market

In order to arbitrage away the risk of those 200,000 VIX futures contracts, the sellers will need to sell options against the SPY or other S&P 500 index proxies. Alternatively, they can sell stocks in the S&P 500 directly. In fact, they can use any of the three other methods mentioned above, in order to reduce their risk. They’ll likely use all three.

What all of this means is a massive flood of selling pressure will likely begin in the stock futures market before the market opens tomorrow morning. This futures selling will then lead to actual stock selling at the open, leading to a massive stock market crash.

This forced liquidation of XIV could then function very similarly to the portfolio insurance phenomenon that caused the -22% single-day drop in October 1987 on Black Monday. Forced selling will feed more forced selling, and the sheer volume of sell orders can overwhelm the available buying liquidity.

Conclusion: XIV Short Volatility Liquidation creates a Margin Call which cascades to both retail and institutional investors selling in strength causing a Stock Market Crash